Digital Payments vs Cash in India: Which Is Better for My Daily Spending (2025-Guide)

Let’s be honest — digital payments have made life unbelievably easy.

No queues, no change“ do you have ₹10 extra?” moments.

A single tap and done.

But here’s the strange part — even though UPI makes life smoother, it’s quietly changing how we feel about money.

Last year, during a short “money awareness experiment,” I tried using only cash challenge for a few days.

And honestly, it shocked me how different it felt.

Pulling out a ₹500 note physically hurt more than tapping “Pay ₹500.”

That’s when I started wondering — why does paying with cash feel so different from UPI?I wanted to test **digital payments vs cash** for real life daily spending and see what actually changes.

This short experiment compares digital payments vs cash

Let’s break it down. 👇

💡 The Core Difference: Tangibility vs Tap – Digital Payments vs Cash

| Factor | Cash Payments | UPI / Digital Payments |

|---|---|---|

| Feeling of loss | Immediate & visible (you see notes leaving) | invisible (just a screen number) |

| Speed | Slow | Instant |

| Awareness | High — you count notes | Low — you just see numbers |

| Spending behavior | More cautious | More impulsive |

Quick look: **digital payments vs cash** — what changes at the moment of payment.

In simple words —

💰 Cash is tangible.

📱 UPI is invisible.

And this small difference changes everything about my spending behavior.

Digital Payments vs Cash — What’s Actually Better for You?

🪙 1. Spending Feels Real with Cash

When comparing **digital payments vs cash**, cash clearly makes spending feel more.

When you hand someone a ₹500 note and get ₹100 back, you actually feel that money leaving your hand 😅.

That moment, It’s good — it stops you from overspending.

But UPI? Tap. Swipe. Gone. — no pain, no pause 😬

🧠 Quick Visual:

| 💵 Cash | 💳 UPI |

|---|---|

| You see the money leave your hand ✋ | You just tap & forget 💨 |

| Helps control impulse spending 🧩 | Makes spending frictionless ⚠️ |

That’s why psychologists say — UPI is like “invisible money.” You spend more because it doesn’t feel like spending.

⚡ 2. Convenience: UPI Wins Without a Fight

Let’s be real — carrying wallets feels so 2010 😅.

UPI is faster, cleaner, and doesn’t need “chillar” change.

You can pay for chai, cabs, groceries — in seconds ⏱️

📊 Mini Comparison:

| Feature | UPI 💳 | Cash 💵 |

|---|---|---|

| Speed | ⚡ Super fast | 🐢 Slow |

| Object | ✅ invisible | ❌ visible |

| Accessibility | 🌍 Works everywhere online | 🏪 Offline only |

But here’s the twist — convenience often hides carelessness. The easier it gets, the less we think before paying 😅.

💡 3. UPI Helps You Track Every Rupee

One big point in the digital payments vs cash debate is that digital gives automatic records — and records build awareness.

This one’s a big win for digital!

UPI keeps auto records 📒 — who you paid, when, and how much.

Cash doesn’t — once it’s gone.

So, if you want to see where your money disappears every month, UPI makes it super easy to track.

🪄 Visual Tip:

Imagine this —

📱 UPI App → ₹99 Swiggy → ₹499 Amazon → ₹45 Chai → ₹220 Uber

💵 Cash → (umm… where did that ₹500 go again?) 😅

Tracking = Awareness.

And awareness = control 🔁

⚠️ 4. UPI Makes Overspending Too Easy

“Just ₹199” — sounds harmless, right?

But you buy three things like that and boom — ₹600 gone before lunch 🍔💸.

With UPI, there’s no pause moment, no second thought.

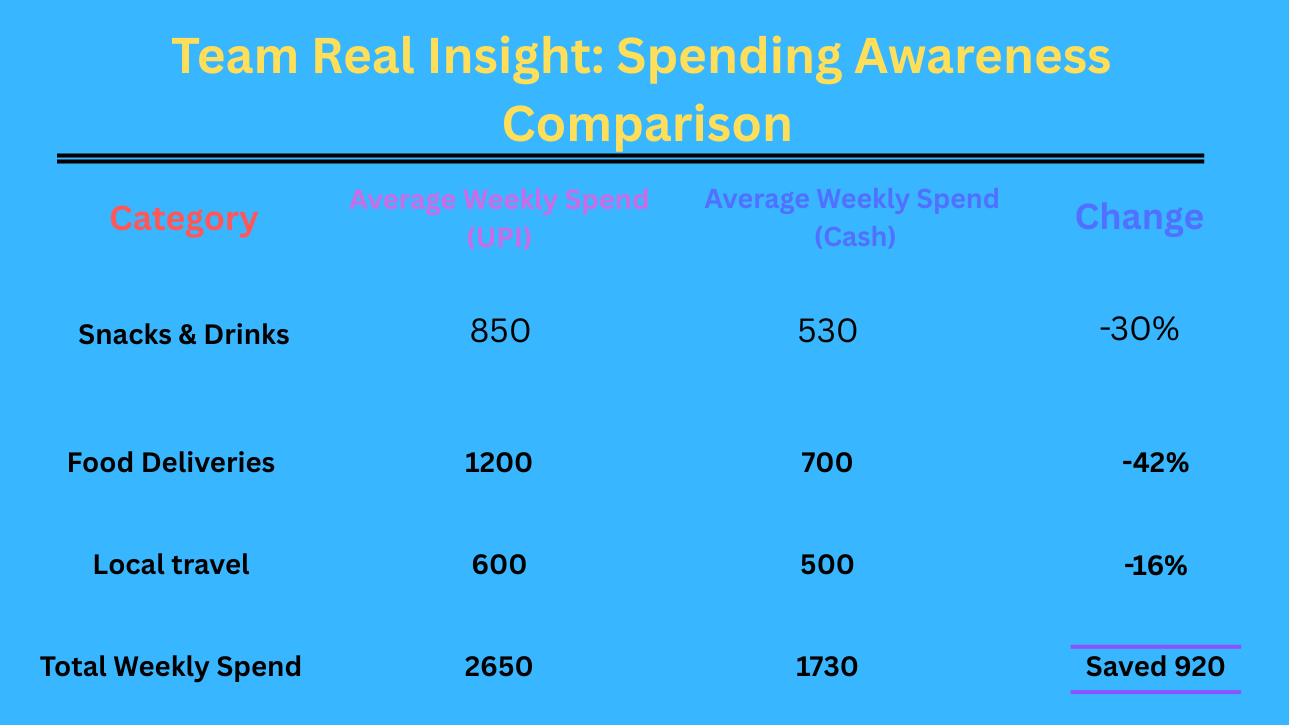

That’s why many people (including us 😅) tried the “One-Week Cash Challenge.”

For 7 days, we used only cash — and realized how differently we spend when we feel the money leave our hands.

🧩 Quick Lesson:

| Habit | UPI Users 💳 | Cash Users 💵 |

|---|---|---|

| Check balance before buying? | Rarely 😅 | Always ✅ |

| Impulse buys | High ⚠️ | Low ✅ |

| End-of-day awareness | “Wait, what did I buy?” 🤔 | “I have ₹200 left!” 💪 |

Also we did a 30 day micro-saving challenge. Where I save ₹5000 in just one month.

The Sweet Spot — Use Both Smartly

The smart answer to ” digital payments vs cash” is not choosing only one.

UPI isn’t bad. Cash isn’t old.

They’re just tools — you gotta use both wisely.

Think of it like this 👇

🔹 Use UPI for: bills, travel, online orders, and budgeting apps.

🔹 Use Cash for: personal limits, small spends, and self-control training.

💬 Because real money awareness isn’t about what you use — it’s about how you use it.

✨ Summary Snapshot

| 🧭 Category | 🪙 Cash | 📱 UPI |

|---|---|---|

| Spending Control | 💪 High | ⚠️ Low |

| Speed & Ease | 🐢 Slow | ⚡ Fast |

| Expense Tracking | ❌ Manual | ✅ Automatic |

| Overspending Risk | 🔒 Low | 🚨 High |

| Best For | Self-control, saving goals | Bills, instant payments |

🪜 A Simple Experiment: “Digital Payments vs Cash”

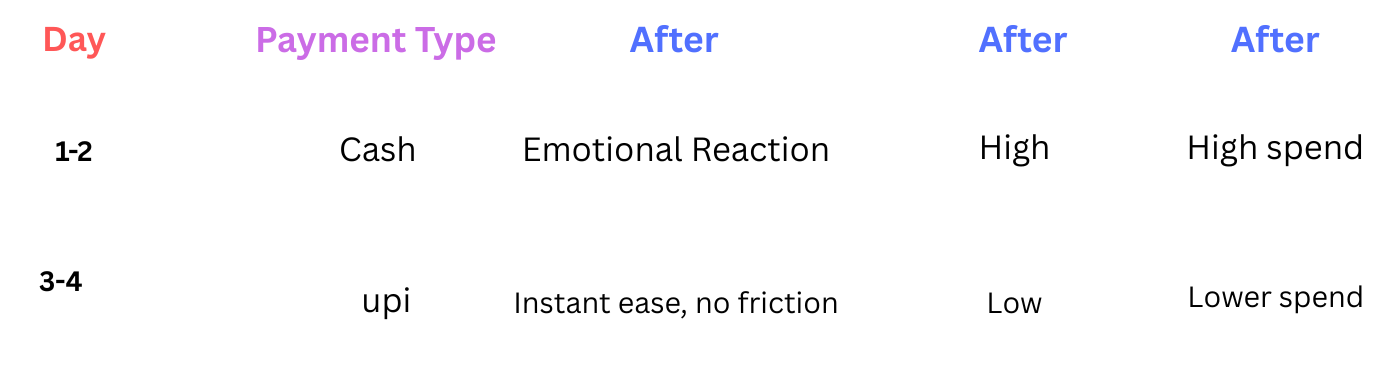

We ran a small test to compare **digital payments vs cash** for daily spending and the results were eye-opening.

Spend 2 days using only cash, and then 2 days using only UPI.

Track both experiences.

I realize, i spend 20–30% more during UPI-only days — not because things cost more, but because i don’t feel the spending.

🧠 The Psychology Behind It – Why i overspend using digital payments

And before you realize, you’ve spent on something you never needed — that’s the hidden side of Digital Payments vs Cash we rarely talk about.

⚡ 1. The Illusion of Effortless Money

UPI makes paying too easy.

No wallet. No counting. No hesitation. Just tap and done.

But that “ease” quietly steals one important habit — the pause.

The few seconds before paying when you’d usually ask yourself:

“Do I really need this right now?”

That pause used to save us from half the unnecessary spends in a month.

💰 2. The Micro-Spending Trap

This one hit me hardest.

₹49 app trials. ₹79 snacks. ₹149 rides. ₹199 “flash sales.”

Each feels harmless — but together, they bleed your wallet dry.

Digital payments make small spends invisible.

You don’t see money leaving, so your brain thinks —

“It’s fine, it’s just a little.”

But when I switched to cash for a week, I could feel every ₹50 note leave my hand.

And suddenly, I started saying “no” more often.

📊 Mini Insight:

| Type of Spend | With Cash | With UPI |

|---|---|---|

| Awareness | High | Low |

| Control | Manual but mindful | Instant but impulsive |

| Emotional Feel | Slight pain | No emotion |

| Long-Term Habit | Conscious saving | Passive overspending |

📲 3. The Notifications & Offers Game

Brands know our psychology better than we do.

That “Flash Sale” or “₹50 Cashback” ping? It’s designed to trigger urgency.

It’s called the FOMO Effect — fear of missing out.

Your brain sees the offer, releases dopamine, and convinces you —

“If I don’t grab it now, I’ll lose something.”

And before you realize, you’ve spent on something you never needed.

💬 FAQ (Frequency Asked Questions)

Q: Should I stop using UPI completely?

A: Instead learn when to prefer ** digital payments vs cash** so you get the benefits of both.

Q: What if I can’t carry cash everywhere?

A: Keep a ₹500–₹1000 wallet buffer for small spends. Use UPI for the rest.

Q: Does cash really reduce spending that much?

A: Yes. Studies show people spend 12–30% less when paying in cash because they feel the “loss” more vividly.

Conclusion

At the end of the day, I’m not saying digital payments are bad — not at all.

They’ve made my life faster, safer, and honestly… way more convenient. 💳⚡

But somewhere between all those “Pay Now” buttons and cashback notifications,

I realized I’d forgotten what real spending actually feels like.

I still remember that little sting when I used to hand over a ₹500 note —

and now? A quick scan, a beep, and it’s gone before I even think twice. 😅

Over time, I’ve learned something simple:

👉 It’s not about picking sides in the Digital Payments vs Cash debate.

👉 It’s about being mindful every single time money leaves my account.

We’re not professionals— just regular people trying to build better money habits. This post shares personal experiences and ideas that worked for us. For more useful advice, check out our Telegram channel.